Initiating Coverage | Logistics

February 21, 2015

Transport Corporation of India

BUY

CMP

`250

Economic revival to spur growth

Target Price

`293

Investment Arguments

Investment Period

12 Months

Top-line growth to accelerate to 15% CAGR over FY2014-17E on economic

Stock Info

revival; eventual GST implementation would provide further boost: We expect

Sector

Logistics

Transport Corporation of India (TCIL) to report a healthy top-line growth ~15%

Market Cap (` cr)

1,890

CAGR over FY2014-17E on the back of revival in the Indian economy. Among

TCIL’s four business segments, we expect (a) Express segment to report ~17%

Net Debt (` cr)

285

CAGR. TCIL is also be well-placed to garner e-commerce business, as bulkier

Beta

1.6

categories like furniture, white goods see more traction in online sales. (b) Supply

52 Week High / Low

299 / 88

Chain Solution segment to report ~21% CAGR, owing to recovery in the

Avg. Daily Volume

15,533

automobile sector, growth in E-commerce fulfillment hubs, as well `as new

Face Value (`)

2

customer wins due to increasing outsourcing of supply chain in other sectors like

BSE Sensex

29,231

FMCG, chemicals, cold storage, etc. especially once GST kicks in. The other two

Nifty

8,834

segments, viz. Seaways and Freight, are also likely to benefit from economic

Reuters Code

TCIL.BO

revival and expected to report ~9% CAGR.

Bloomberg Code

TRPC@IN

Stepped-up capex spending in higher margin businesses to aid overall earnings

growth trajectory: As the demand environment improves, we expect margins to

Shareholding Pattern (%)

improve across segments for TCIL. Moreover, we expect the company to increase

Promoters

69.1

focus on higher margin businesses like XPS and Supply Chain Solution. As a

MF / Banks / Indian Fls

0.8

result, the revenue contribution of these businesses is expected to increase from

FII / NRIs / OCBs

2.3

~56% in FY2014 to ~62% in FY2017E, with the company having aggressive

Indian Public / Others

27.9

expansion plans in these businesses (Rs500cr capex over FY2015-17E). As a

result, we expect overall margins to improve from 7.6% in FY2014E to 9.0% in

Abs. (%)

3m 1yr

3yr

FY2017E, driving 25% CAGR in net profits over the same period.

Sensex

4.2

42.3

59.8

Outlook and Valuation: TCIL benefits from its pan-India scale (which gives it

TCIL

(3.9) 182.5

247.3

competitive advantage in higher margin segments of the logistics industry) as well

as from its asset-light business model (which cushions its profitability in cyclical

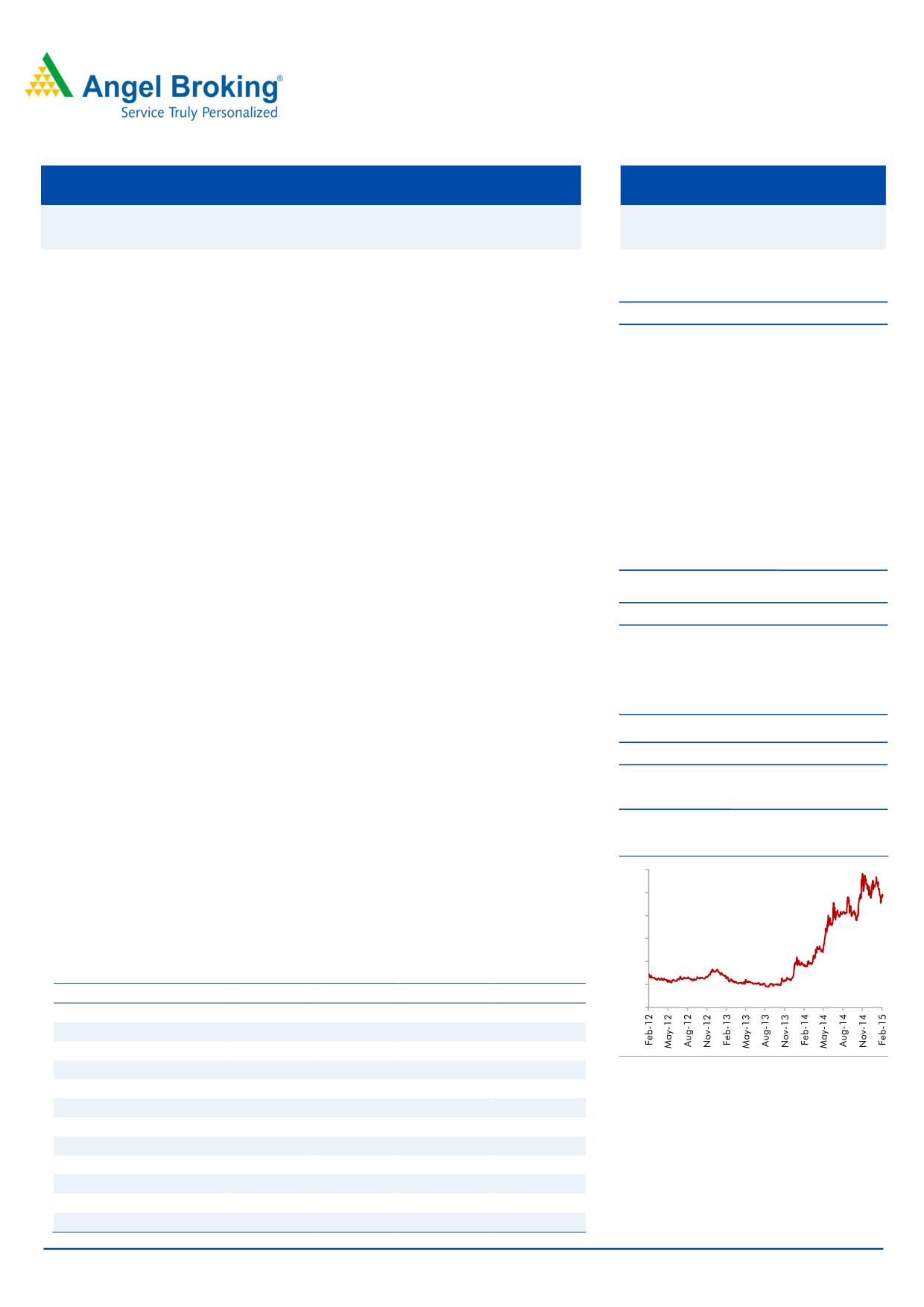

3-year price chart

downturns and gives it an attractive ROE profile). The company is well-placed to

300

be a key beneficiary once GST is implemented, when corporates will need reliable

250

pan-india logistics players to manage their hub-and-spoke supply chains. At the

200

CMP, TCIL trades at a P/E of 13.7x FY2017E. We initiate with a Buy and target

150

price of `293 (16x FY2017E EPS), indicating an upside of ~17%.

100

Key financials

50

Y/E March (` cr)

FY2014

FY2015E

FY2016E

FY2017E

0

Net sales

2,228

2,468

2,830

3,350

% chg

4.5

10.8

14.6

18.4

Net profit

72

87

109

138

% chg

3.0

22.1

24.3

27.4

Source: Company, Angel Research

EBITDA margin (%)

7.6

8.0

8.8

9.0

EPS (`)

9.5

11.6

14.4

18.3

P/E (x)

26.4

21.6

17.4

13.7

P/BV (x)

3.9

3.0

2.7

2.3

RoE (%)

14.6

14.1

15.4

17.1

RoCE (%)

14.9

14.2

16.4

18.0

Amarjeet S Maurya

EV/Sales (x)

1.0

0.9

0.8

0.7

022-39357800 Ext: 6831

EV/EBITDA (x)

12.8

10.9

8.9

7.6

Source: Company, Angel Research, Note: CMP as of February 20, 2015

Please refer to important disclosures at the end of this report

1

Transport Corporation of India | Initiating Coverage

Investment Arguments

E-commerce industry to drive growth of XPS division

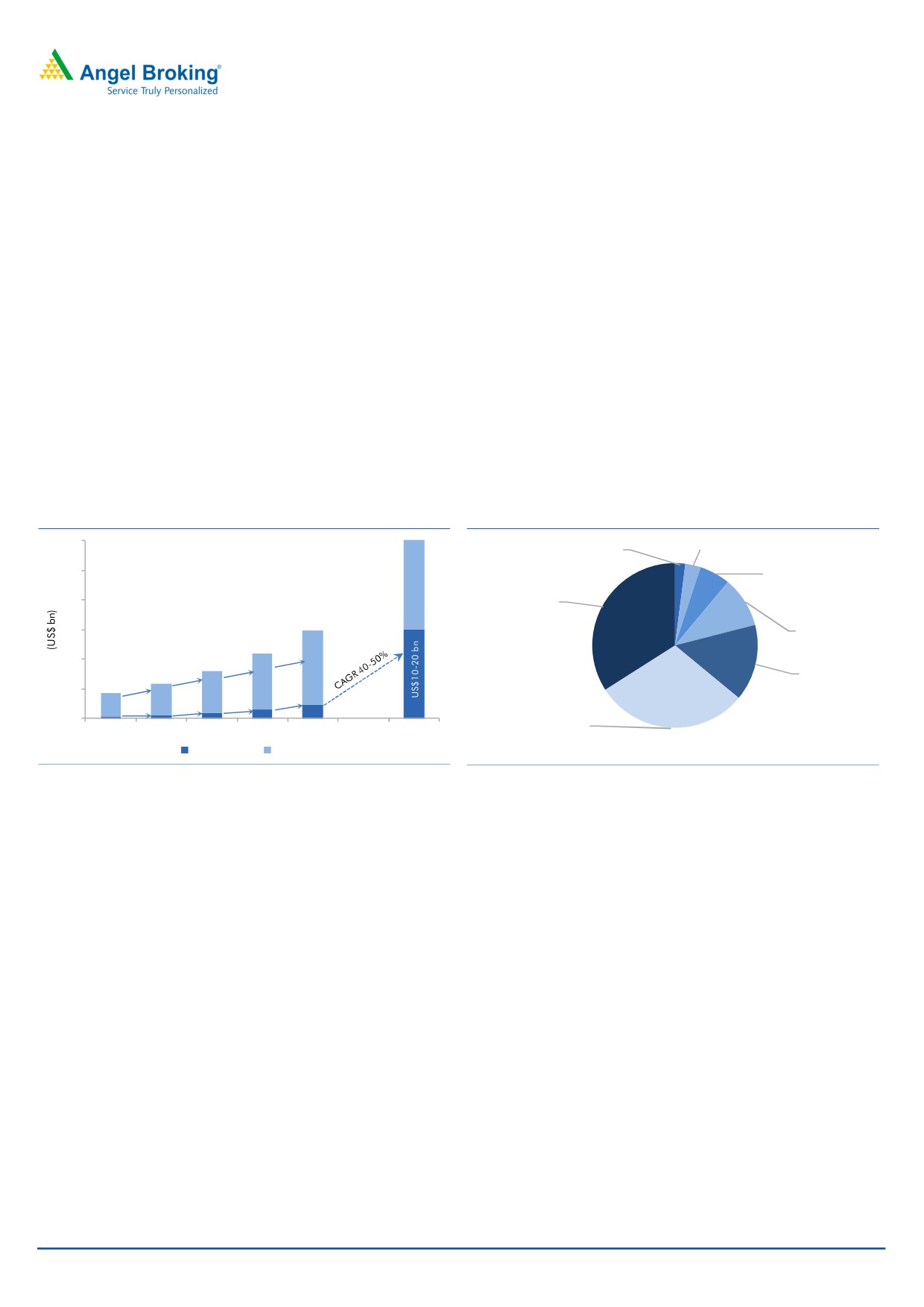

According to ASSOCHAM and PWC, the Indian e-commerce industry’s market size

is less than 10% of USA and China’s market size (US$150bn) of ecommerce.

Indian e-commerce industry’s market

However, over 2009-13, the e-commerce sector in India has grown at a CAGR of

size is less than 10% of USA and China

almost 35% to an estimated US$12.6bn on back of rising internet and mobile

market size (US$ 150bn) of ecommerce.

phone penetration. In the domestic e-commerce industry,

~70% of the

transactions are accounted by online ticketing and ~10% by e-retailing and online

market place. However, e-retail in both its forms, ie online retail and market place,

has become the fastest-growing segment, increasing its share from 10% in 2009 to

an estimated 18% in 2013. As per an industry report, going forward, the e-retail

market is expected to grow to around US$10-20bn by 2017-20 on account of

increase in consumer-led purchases in durables and electronics, apparels and

accessories etc.

Exhibit 1: Growth in e-commerce & e-tailing (e-retail)

Exhibit 2: Product mix in e-tailing

30

Baby products,

Healthcare ,

2%

3%

Home and

25

furnishing , 6%

20

Electronics ,

34%

Beauty &

15

personal , 10%

29%

10

32%

12.6

Books , 15%

29%

37%

9.5

5

7.0

5.3

53%

3.8

58%

53%

57%

1.0

1.5

2.3

0.4

0.6

0

Apparels &

2009

2010

2011

2012

2013

2017-20

accessories ,

E-Commerce E-Tailing

30%

Source: Crisil, IAMAI, PwC analysis and Industry experts

Source: Internet and Mobile Association of India research

Robust growth in e-retailing over the last few years is aiding growth for logistics

companies. Going forward, we believe that growth in e-retail would trigger growth

TCIL’s XPS division (express delivery of

of the express business of logistics companies. TCIL’s XPS division (express delivery

goods) accounted for ~29% of FY14

of goods) accounted for ~29% of the company’s FY2014 revenues. In this

revenues.

segment, the company’s focus is on both B2B and B2C (both being a part of

e-commerce). TCIL’s 50% revenue comes from apparels, pharma and electronic

goods. Currently, TCIL is generating negligible revenue from ecommerce; the

revenue from ecommerce as a proportion of total revenue is very low. The

companies is also into movement of large white goods such as televisions,

refrigerators etc, which are still not preferred to be bought from e-commerce

platforms by customers. In our view, growing customer preference for buying large

white goods online will drive growth for the company in the long term. Further, the

company also provides services towards moving consumer durables and electronic

equipment from facilities of the OEMs to warehouses of e-tailing companies. TCI

also operates fulfillment centres for e-tailing companies and has plans to scale up

these services going forward.

February 21, 2015

2

Transport Corporation of India | Initiating Coverage

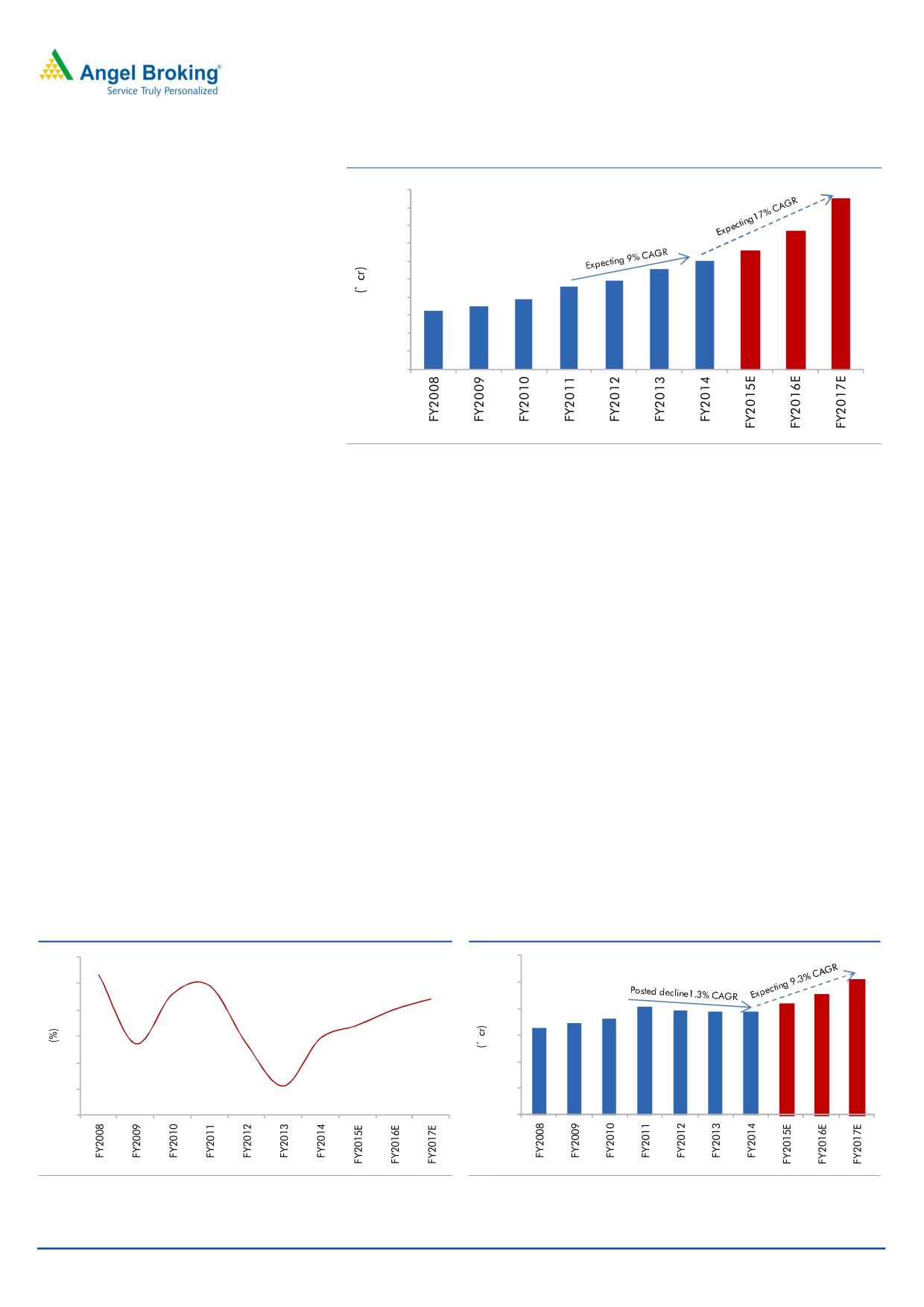

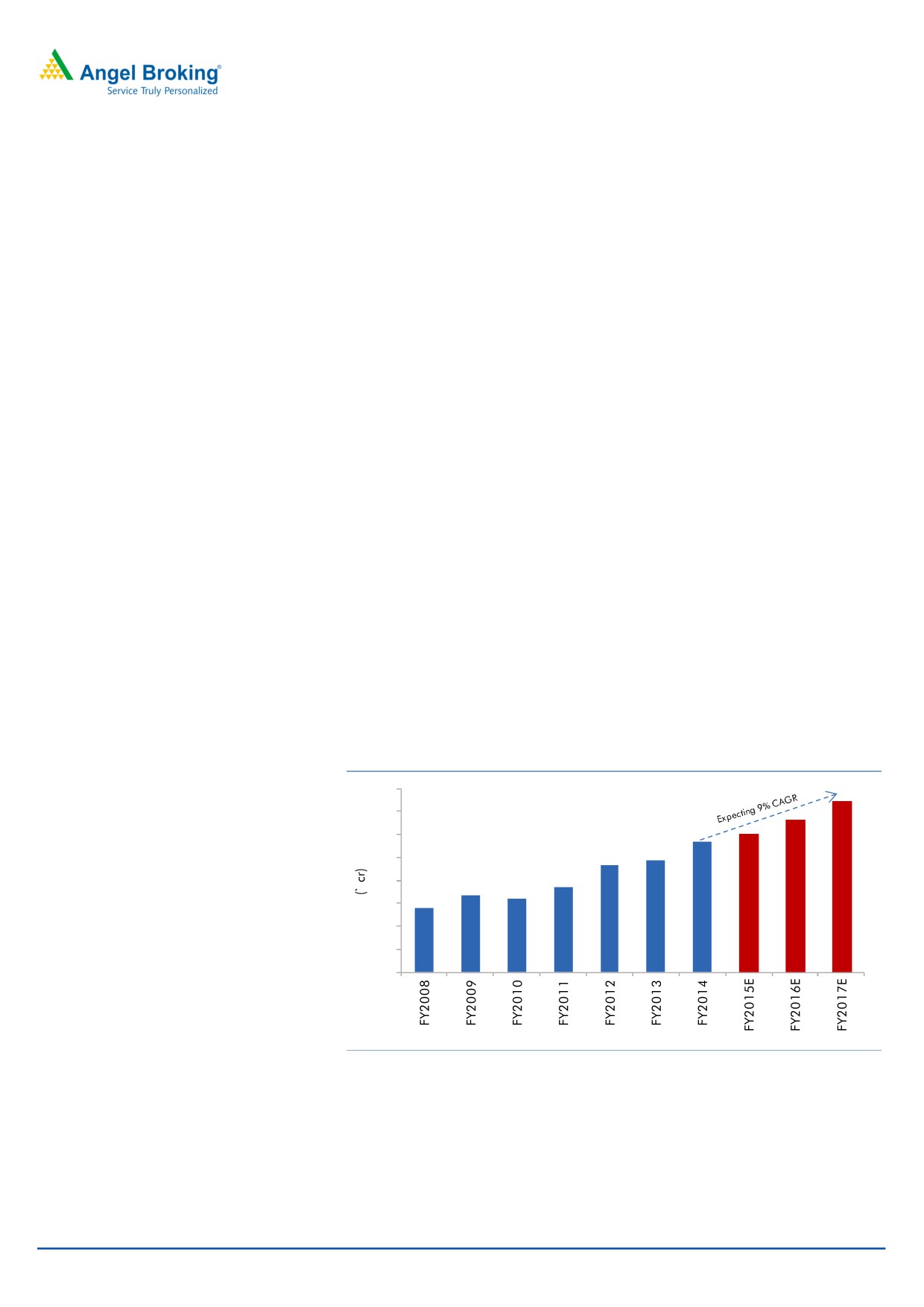

Exhibit 3: Projected Revenue growth trend for XPS Division

1,000

In XPS division, we expect the company

900

800

to report a strong ~17% CAGR over

700

FY2014-17E

600

500

400

300

200

100

-

Source: Company, Angel Research

Hence, considering growth in 9MFY2015 sales numbers, improvement in

economy, strong growth in e-commerce segment, and capacity expansion, we

expect the company to report a strong ~17% CAGR over FY2014-17E.

Economic revival to boost the growth for Freight division

In the freight segment, the company is one of India’s premier organized freight

services providers with a pan India presence. The company has around 2,400

trucks and trailers, both owned and leased, which provide freight movement

services on a daily basis. It has a strong backing in terms of its extensive and

strategically located branch network and trained work force. The Freight division

contributes by ~38% (FY2014) to the total revenue. TCIL’s Freight division

(Transport division) has been underperforming in the last few years (it reported a

de-growth of ~1% [CAGR] over FY2011-14) due to slowdown in GDP growth,

reflecting slowdown in overall industrial activity in the country. In 9MFY2015, the

Freights division showed recovery in revenue growth, ie it posted a revenue growth

of ~5% yoy (mainly in the previous quarter), owing to an improving economic

scenario. Further, the Management is also confident of posting a better

performance, than in the previous few quarters, in the coming financial years.

Exhibit 4: GDP growth expected to bounce back

Exhibit 5: Projected Revenue growth trend for Freight division

10

1,200

9

1,000

8

800

7

600

6

400

5

200

4

-

Source: Company, Angel Research

Source: Company, Angel Research

February 21, 2015

3

Transport Corporation of India | Initiating Coverage

Considering momentum in policy reforms, fall in inflation, and anticipation of

further rate cuts by the Reserve Bank of India (RBI), we believe that the investment

cycle and commercial activities in the country will get a boost. This would lead to

We expect the Freight division to report

improvement in GDP growth in FY2016 and FY2017, which in turn will assist

a healthy ~9% CAGR over FY2014-17E

overall growth in the Freight division (Transport segment). Also, industry is

expecting GST implementation in FY2016 which will further increase the growth

prospects of the industry, and this will directly benefit the company with it being a

dominant player in the industry. Considering the overall improvement in demand

for the Freight division in 9MFY2015, increasing numbers of trucks in operation,

and improving economy activities, we expect the Freights division to report a

healthy ~9% CAGR over FY2014-17E.

Recovery in automobile industry to aid Supply Chain Solution

(SCS) division

The automobile industry’s performance in the past two consecutive years (FY2013

and FY2014) has been disappointing. But in 9MFY2015, the 2W industry has

~75% of Supply Chain Solution

reported a strong growth of ~13% due to recovery in domestic and export

division’s

business

comes from

markets, and passenger vehicle (PV)s have also shown an ~4% yoy growth.

Automobile sector and balance from

Further, the commercial vehicle (CV) segment has also shown some improvement

FMCG

(de-growth of ~4% yoy for 9MFY2015 as against a ~19% yoy de-growth for

FY2014) on back of improvement in sales volumes in medium and heavy

commercial vehicle (MHCV) and light commercial vehicle (LCV) segments. We

expect growth momentum to continue and expect the Indian automobile industry to

report a healthy 12.5% CAGR over FY2014-17E.

Exhibit 6: Expected revival in Automobile industry

Exhibit 7: Projected Revenue growth trend for SCS division

1,200

35

30

1,000

25

800

20

600

15

400

10

200

5

0

0

Source: SIAM, Angel Research

Source: Company, Angel Research

The Supply Chain Solution segment accounts for ~27% of total revenue (FY2014)

of TCIL. In this segment ~75% of the business comes from the automobile sector

TCIL’s marquee customers include

and the balance from the FMCG and other segments (marquee customers include

Maruti, GM, Tata Motors, Hero, Bajaj,

Maruti, GM, Tata Motors, Hero, Bajaj, Hindustan Unilever, Samsung, VW Group

Hindustan Unilever, Samsung, VW

etc). In the segment, the company caters to automobile OEMs; it provides supply

Group etc

chain solutions including inbound logistics, outbound logistics, and stocking

vehicles at the warehouses. Further, in this segment, the company has a JV with

Mitsui, Japan which manages the entire inbound logistics operations of Toyota

Kirloskar Motors India since 1999. The company owns 49% stake in this JV. Apart

February 21, 2015

4

Transport Corporation of India | Initiating Coverage

from this, the company also provides services in managing fulfillment centers and

back-end operations for e-commerce.

During FY2014, the division’s revenue was impacted due to slowdown in the

automobile industry. During 9MFY2014, TCIL has already reported a strong

growth of ~16% against ~4% growth for the same period last year, on back of

improvement in automobile industry sales volume numbers. Going forward, in our

view, we expect the automobile industry to report strong numbers on back of

improvement in the economy and expected interest rate cuts which would directly

benefit TCIL. Further, the company is also increasing capacity of its warehousing

facilities to cater to other verticals/sectors such as chemicals, temperature, etc.

Hence, considering this, we expect the Supply Chain Solution segment to report a

strong ~21% CAGR in revenue over FY2014-17E.

Capacity expansion of Seaways division to drive growth

TCI Seaways has well equipped ships in its fleet and caters to the coastal cargo

requirements for transporting container and bulk cargo from ports on the East

In Seaways division, we expect the

coast of the country. Recently, the company has increased its fleet from 4 ships in

company to report a strong revenue

FY2014 to 5 ships during 9MFY2015; also, it has replaced one ship. As a result

CAGR of ~9% over FY2014-17E

the total capacity has increased from ~17,000 DWT to ~27,800 DWT.

Further, the company is also planning to diversify outside Port Blair sector and

operate on the west coast as well. With the additional capacity of ships, the

company can generate `50-60cr revenue with an EBITDA margin of 10-15%,

translating into a healthy return ratio. Going forward, we expect the company to

report a strong ~9% CAGR in revenue over FY2014-17E.

Exhibit 8: Projected Revenue growth trend for Seaways division

160

140

120

100

80

60

40

20

0

Source: Company, Angel Research

February 21, 2015

5

Transport Corporation of India | Initiating Coverage

GST implementation to benefit the logistics sector

India’s duty and taxation system is very complex and expensive due to 29 states

and seven union territories which resulted into burden on intra-India trade. Indian

duty and tax structure differ from city to city, thus creating headwinds for creation

of national networks. We believe that the introduction of the Goods and Services

Tax (GST) would benefit the logistics sector. However, we are expecting

implementation of GST only by CY2016. In our view, TCIL over the years has

increased its presence across the country. In a scenario, where GST gets rolled-out,

we expect TCIL to be one of the few pan-India based Logistics players to get

benefitted from any such development.

Stepped-up capex spending in higher margin business to aid

overall earnings growth trajectory

38% of TCIL’s revenue comes from the Freights division, which is a low margin

business (3-5% margin on EBITDA level). Margins are low with the business being

mature and fragmented. Entry barriers are low owing to it not being a capital

intensive business. We expect the revenue contribution of the Freight division to

We expect the company’s higher

come from ~38% in FY2014 to ~33% in FY2017E with the company’s lower focus

margin businesses ie XPS and Supply

on the business. Going forward, we expect the company’s higher margin

Chain Solution to increase their revenue

businesses ie XPS (8-10% margin on EBITDA level) and Supply Chain Solution

contribution from ~56% in FY2014 to

(10-12% margin on EBIDTA level) to increase their revenue contribution from

~62% in FY2017E

~56% in FY2014 to ~62% in FY2017E, led by aggressive expansion plans in

these businesses.

Exhibit 9: Capital Expenditure Plan for the period

(` cr)

FY2007-14

FY2015-17

9MFY2015

Hub Centers & Small warehouses

219

280

40

The company spending

~76% of

Wind power

9

-

-

capex for XPS and Supply chain

Ships & Containers

74

118

70

Solution businesses

Trucks & Cars

220

88

15

Others

65

14

5

Total

586

500

130

Source: Company, Angel Research

We expect the XPS business to perform better on back of improvement in economy

and increase in penetration of e-commerce. The Supply Chain Solution business is

also expected to do well and achieve strong growth due to recovery in Indian

automobile industry. Also, in this business, the company is expected to add new

clients in the FMCG, chemicals, temperature and other segments and expect the

business to benefit from the implementation of the GST. Also, the company would

be incurring significant capex towards building warehouses, which would drive

growth.

February 21, 2015

6

Transport Corporation of India | Initiating Coverage

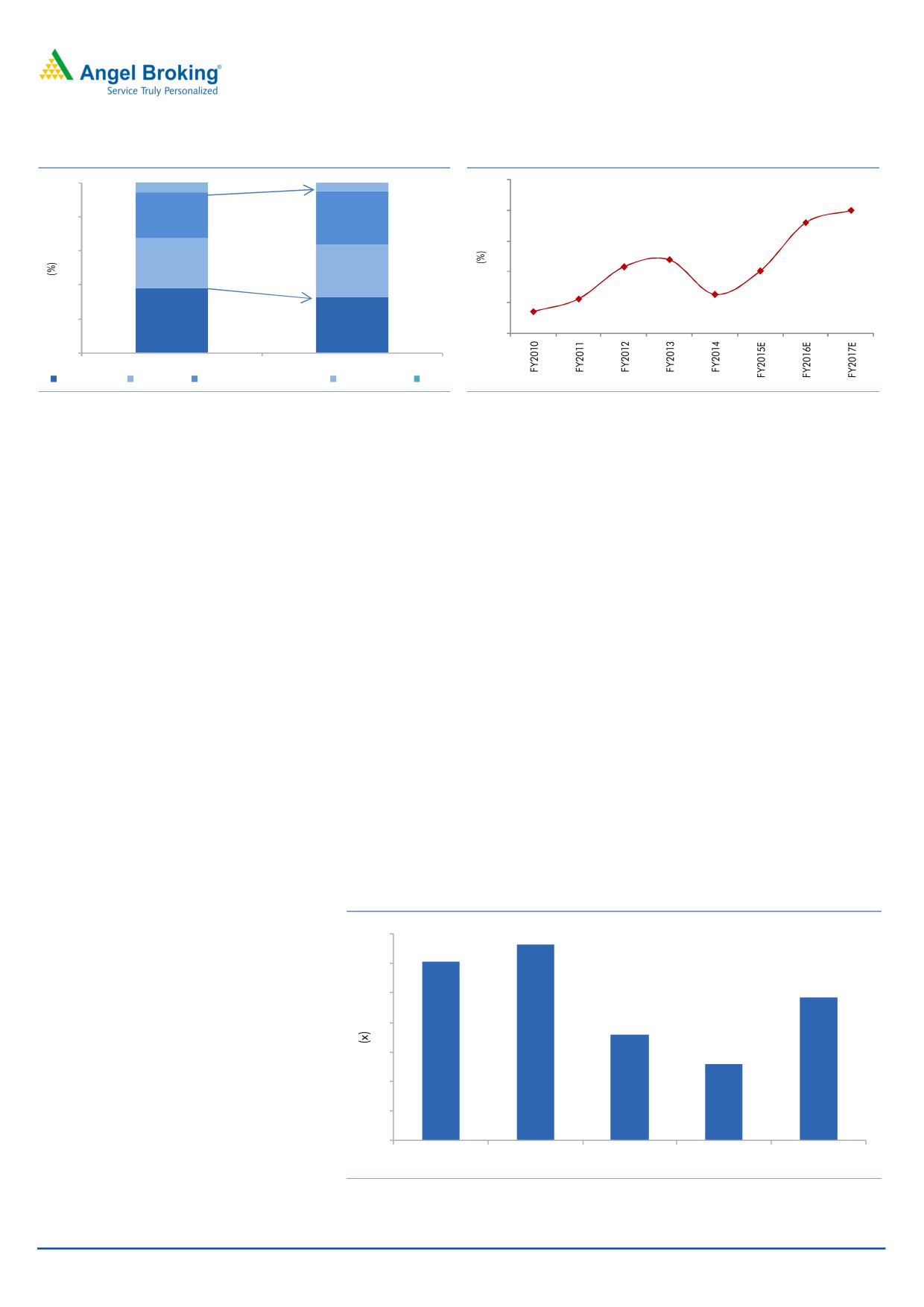

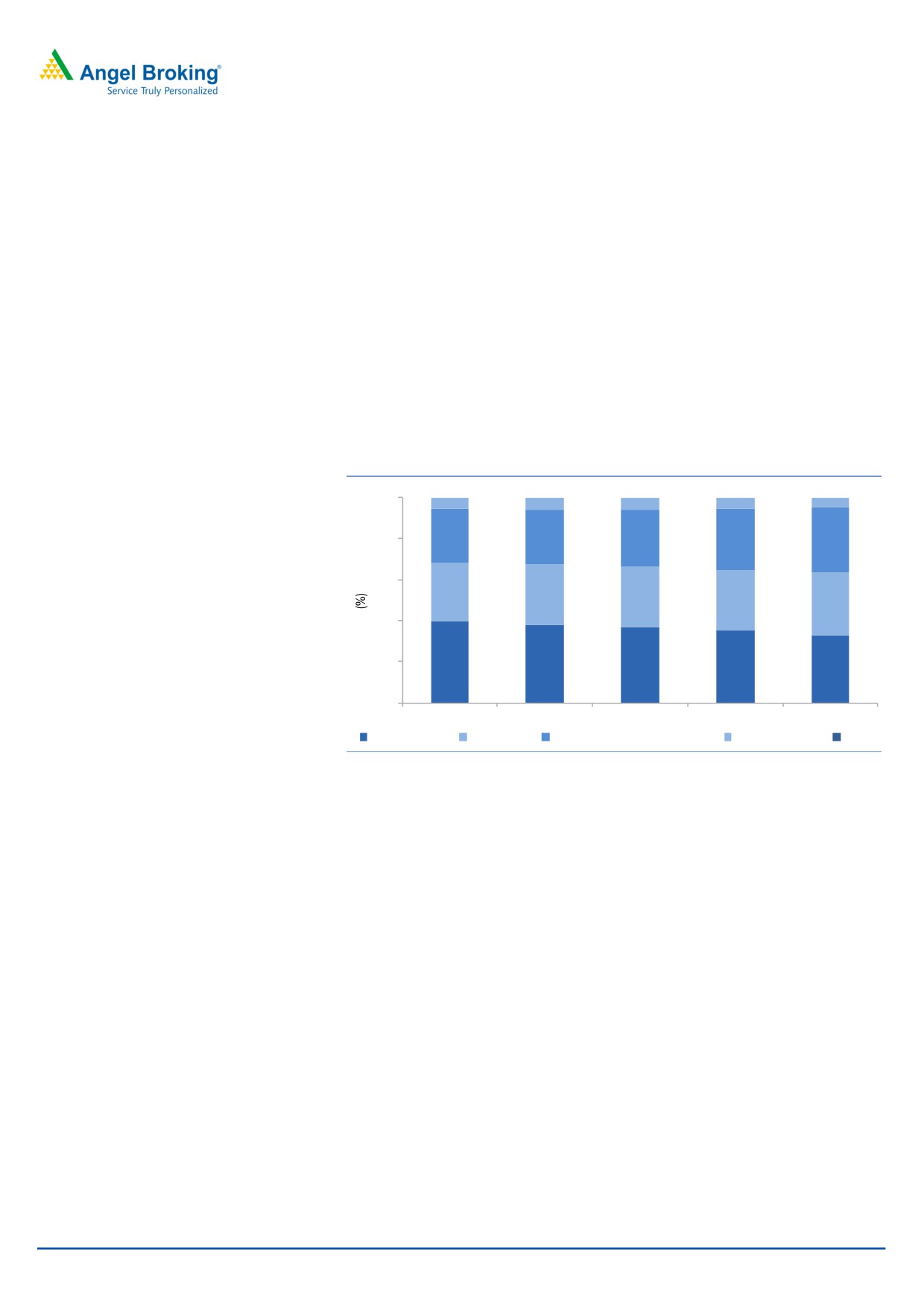

Exhibit 10: Sales tilt towards high margin business

Exhibit 11: Operating margins to expand

100

10

6

5

9.0

9

8.8

80

27

31

9

8.2

60

8.1

8.0

29

31

8

7.6

40

7.6

7.3

8

20

38

33

7

0

FY2014

FY2017E

Freight Division

XPS Division Supply Chain Solution Division Seaways Division Others

Source: Company, Angel Research

Source: Company, Angel Research

Hence, considering the above factors and with the company having reported

strong revenue growth for 9MFY2015 (coupled with margin improvement in some

of its divisions), we expect the company’s overall operating margin to improve

along with an improvement in the return ratio.

Well positioned due to its Asset light business model

TCIL operates on an asset light business model where it owns 20% of the total fleet

and leases the remaining 80%. The company has fastly scaled its business model

to 7,000 trucks/trailers/reefer vehicles as of today. On the same lines, TCIL has

been prudent in managing warehousing space, as a majority of its total 10mn sq ft

of warehousing space is on lease basis. With its focus to invest less on building the

asset base, the company has been able to generate healthy return ratios even in

the worst phases of business cycles. Given the company’s unlevered business

model, we are of the view that the long-term growth prospects of the company

would not be impacted due to lack of capital availability.

TCIL is one of the few companies in Surface Transportation & Logistics space,

which has consistency enjoyed a healthy asset turnover (FY2014 asset turnover

ratio at 5.2x) and ROE (FY2014 ROE at 14.6%). Given the strong matrices the

company displays, we are confident that TCIL at any phase of the business cycle

would be well positioned compared to its peers, which have majorly levered

business models and have lower ROEs.

Exhibit 12: Assets turnover ratio trend

5

5.2

5.1

5

5.0

5

5

4.9

5

4.8

5

5

5

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Source: Company, Angel Research

February 21, 2015

7

Transport Corporation of India | Initiating Coverage

Outlook and Valuation

Going ahead, we expect TCIL to report a top-line CAGR of ~15% over FY2014-

We expect TCIL to report a top-line

17E to ~`3,350cr owing to recovery in sales growth. (a) The Freight division is

CAGR

of

~15%

over

expected to benefit due to improvement in industrial activities (b) The XPS Cargo

FY2014-17E to ~`3,350cr

division’s growth would be supported by growth in e- commerce (c) The Supply

Chain Solution division is expected to grow owing to recovery in the automobile

industry (more than 75% of the division’s revenue comes from the automobile

sector) and (d) The Seaways segment would benefit due to addition of new ships.

Also, improvement in the Indian economy would aid overall growth of the

company. Further, TCIL over the years has increased its presence across the

country. In a scenario, where GST gets rolled-out, we expect TCIL to be one of the

few pan-India based Logistics players to get benefitted from any such

development.

On the bottom-line front, we expect the company to report ~25% CAGR over

FY2014-17E on account of healthy top-line growth in the higher margin business

(change in revenue mix). Also we expect an operating margin improvement (60-

70bp) in the Freight segment due to pick up in volumes and lower fuel cost.

Further, TCIL operates on an asset light business model due to that company

would able to generate healthy return ratios even in the worst phases of business

cycles.

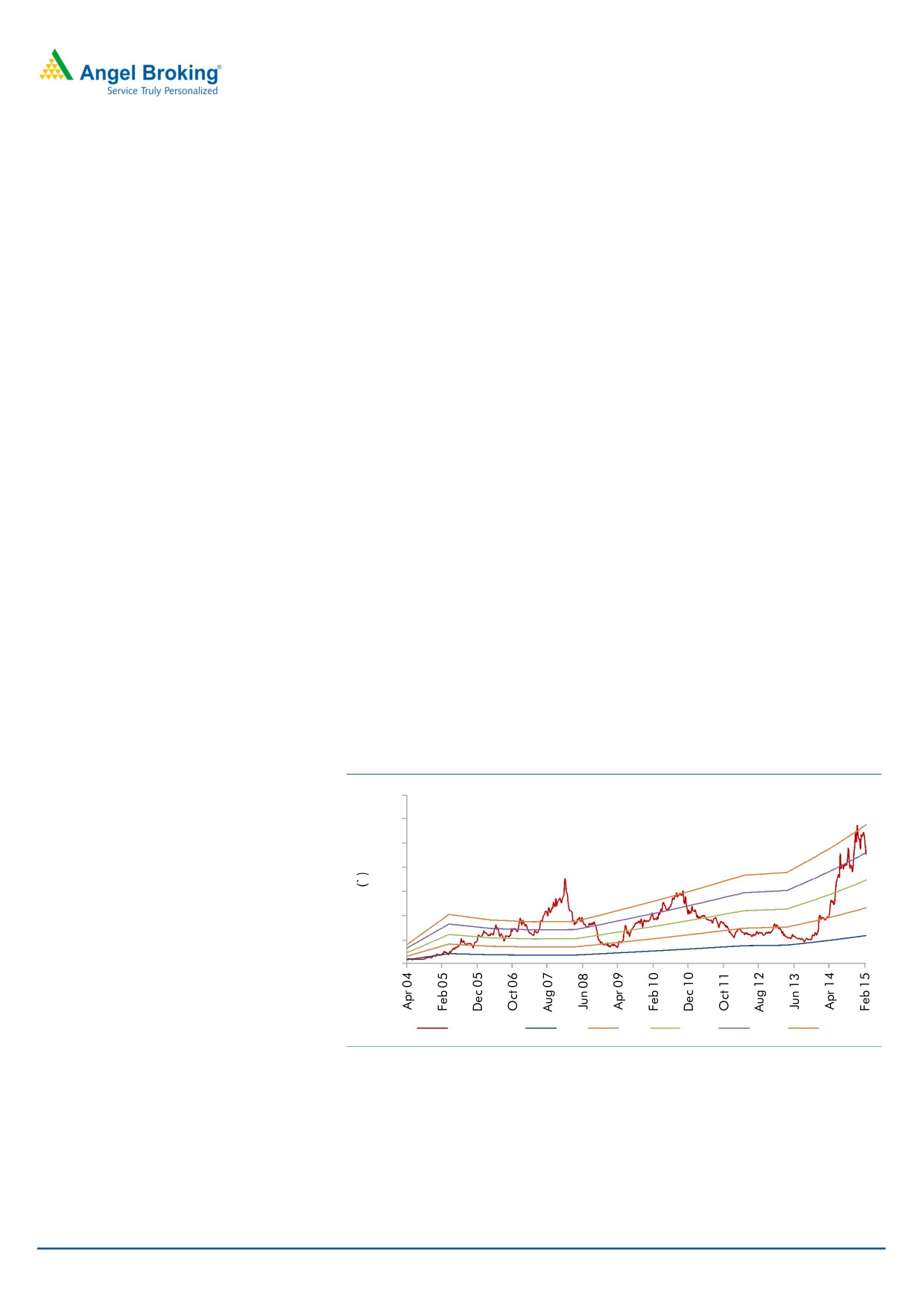

At the current market price of `250, the stock trades at a PE of 17.4x and 13.7x its

FY2016E and FY2017E EPS of `14.4 and `18.3, respectively. We initiate coverage

on the stock with a Buy recommendation and target price of `293, based on 16x

FY2017E EPS, indicating an upside of ~17% from the current levels.

Exhibit 13: One year forward PE chart band

350

300

250

200

150

100

50

0

Share Price

4x

8x

12x

16x

20x

Source: Company, Angel Research, Capitaline

February 21, 2015

8

Transport Corporation of India | Initiating Coverage

Exhibit 14: Comparative analysis

Company

Year end

Mcap

Sales

OPM PAT

EPS

RoE

P/E

P/BV

EV/ Sales

EV/ EBIDTA

TCIL

FY2015E

1,890

2,468

8.0

87

11.6

14.1

21.6

3.0

0.9

10.9

FY2016E

2,830

8.8

109

14.4

15.4

17.4

2.7

0.8

8.9

FY2017E

3,350

9.0

138

18.3

17.1

13.7

2.3

0.7

7.6

Gati

FY2015E

2,199

1,743

10.9

62

7.1

7.8

35.5

3.0

1.6

14.8

FY2016E

2,100

11.8

94

10.7

11.1

23.6

2.7

1.3

11.3

FY2017E

2,523

12.3

125

14.8

13.4

17.0

2.5

1.1

8.9

Source: Consensus, Angel Research

The downside risks to our estimates include 1) Increase in competition

would impact overall growth of the company, 2) Any increase in petrol and diesel

prices could negatively impact profitability (mainly in the Freight segment),

3) Delay in GST implementation would be a headwind for the industry’s growth

prospects, 4) Delay in plan capital expenditure in company’s segment could

hamper the company’s growth, and 5) lower-than-expected Indian economic

growth could affect company’s growth.

February 21, 2015

9

Transport Corporation of India | Initiating Coverage

Company Background

Transport Corporation of India Limited (TCI) is an integrated supply chain and

logistics solutions provider. The company operates in six business divisions: TCI

Freight, TCI XPS, TCI Supply Chain Solutions, TCI Seaways, TCI Global and TCI

Foundation. TCI Freight offers multimodal transport solutions for cargo of any

dimension. TCI XPS is a door-to-door express distribution specialist. TCI Supply

Chain Solutions provides supply chain solutions and services right from

conceptualization to implementation. TCI Seaways caters to the costal cargo

requirements for transporting container and bulk cargo from parts on the east

coast of India to Port Blair in the Andaman and Nicobar Islands and further

distribution within the islands. TCI Global provides a single window advantage to

its customer across all South East Asian countries.

Exhibit 15: Revenue mix

0

0

0

0

0

100

5

6

5

5

5

80

27

27

28

30

31

60

28

29

29

30

31

40

20

40

38

37

35

33

0

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Freight Division XPS Division Supply Chain Solution Division Seaways Division Others

Source: Company, Angel Research

February 21, 2015

10

Transport Corporation of India | Initiating Coverage

Financial outlook

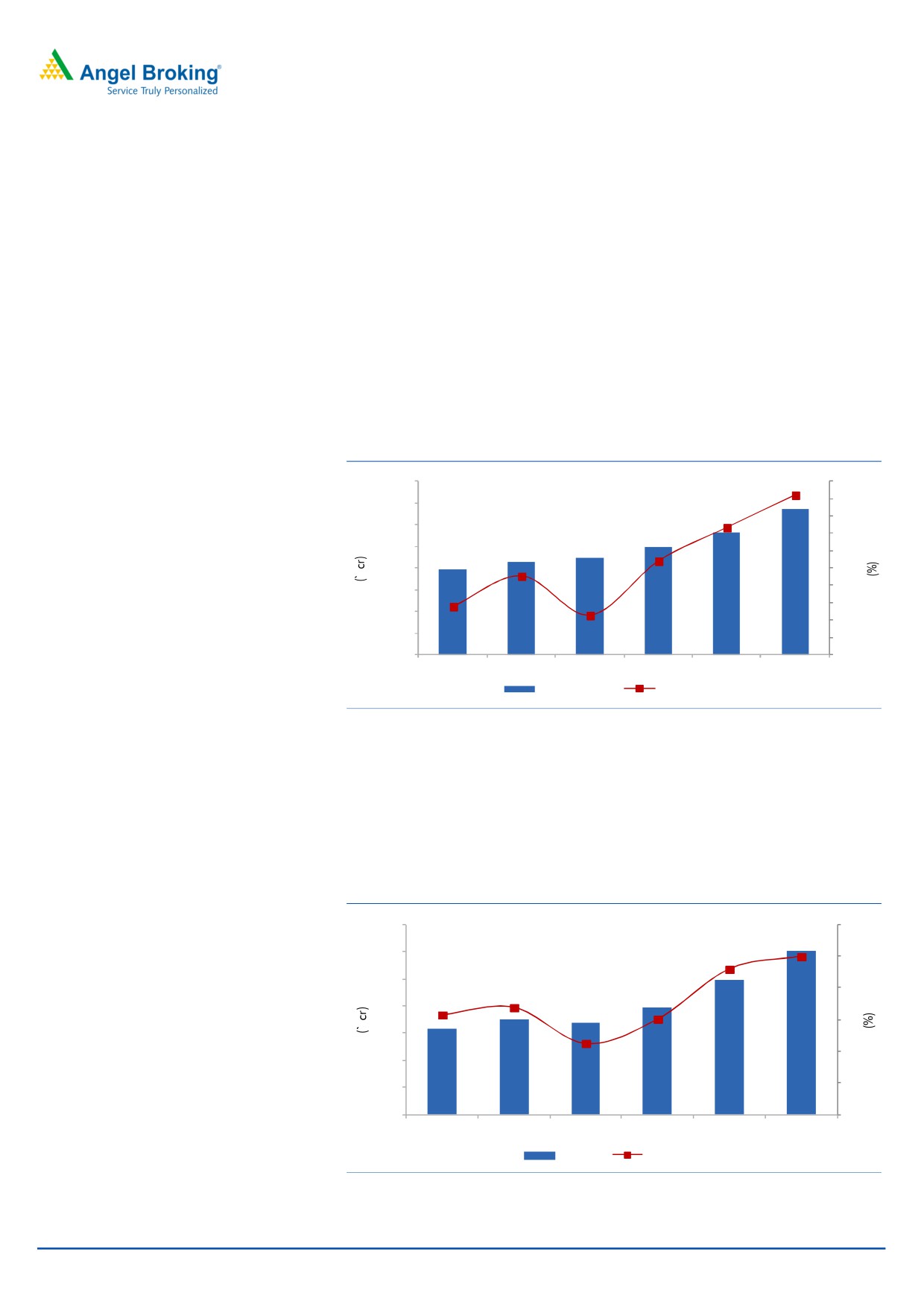

Top-line likely to clock a CAGR of ~15% over FY2014-17E

Going forward, we expect TCIL to

TCIL has reported a consolidated sales CAGR of ~6% over FY2011-14. During

register healthy consolidated top-line

FY2014, the company was unable to perform well due to slowdown in Indian

CAGR of ~15% over FY2014-17E

economy which impacted the overall Freight and XPS segments. Going forward,

we expect TCI to register a healthy net sales CAGR of ~15% over FY2014-17E

supported by healthy sales growth in Freight, XPS, Supply Chain Solution and Ship-

TCISW segments on back of recovery in the Indian economy. Further, we expect

implementation of GST in CY2016 to also boost growth of logistic companies like

TCIL. Hence, we expect TCIL’s net sales to grow by ~15% yoy and ~18% yoy in

FY2016 and FY2017, respectively.

Exhibit 16: Projected Net Sales growth trend

4,000

18.4

20

18

3,500

14.6

16

3,000

14

2,500

10.8

12

9.0

2,000

10

8

1,500

5.5

4.5

6

1,000

4

500

2

-

0

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

Net Revenue

yoy growth (%)

Source: Company, Angel Research

Consolidated EBITDA to witness a CAGR of ~21% over FY2014-17E

Going forward, we expect the

Going forward, we expect the company’s operating margin to be improve from

company’s consolidated EBITDA margin

8% to 9% owing to higher contribution of higher margin businesses like XPS Cargo

to be in the range of 8.0-9.0%

and Supply Chain Solution in total revenue and improvement in utilization.

Exhibit 17: Projected EBIDTA and margin trend

350

10

9.0

300

8.8

9

250

8.2

9

8.1

8.0

200

8

7.6

150

8

100

7

50

0

7

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

EBITDA

Margin (%)

Source: Company, Angel Research

February 21, 2015

11

Transport Corporation of India | Initiating Coverage

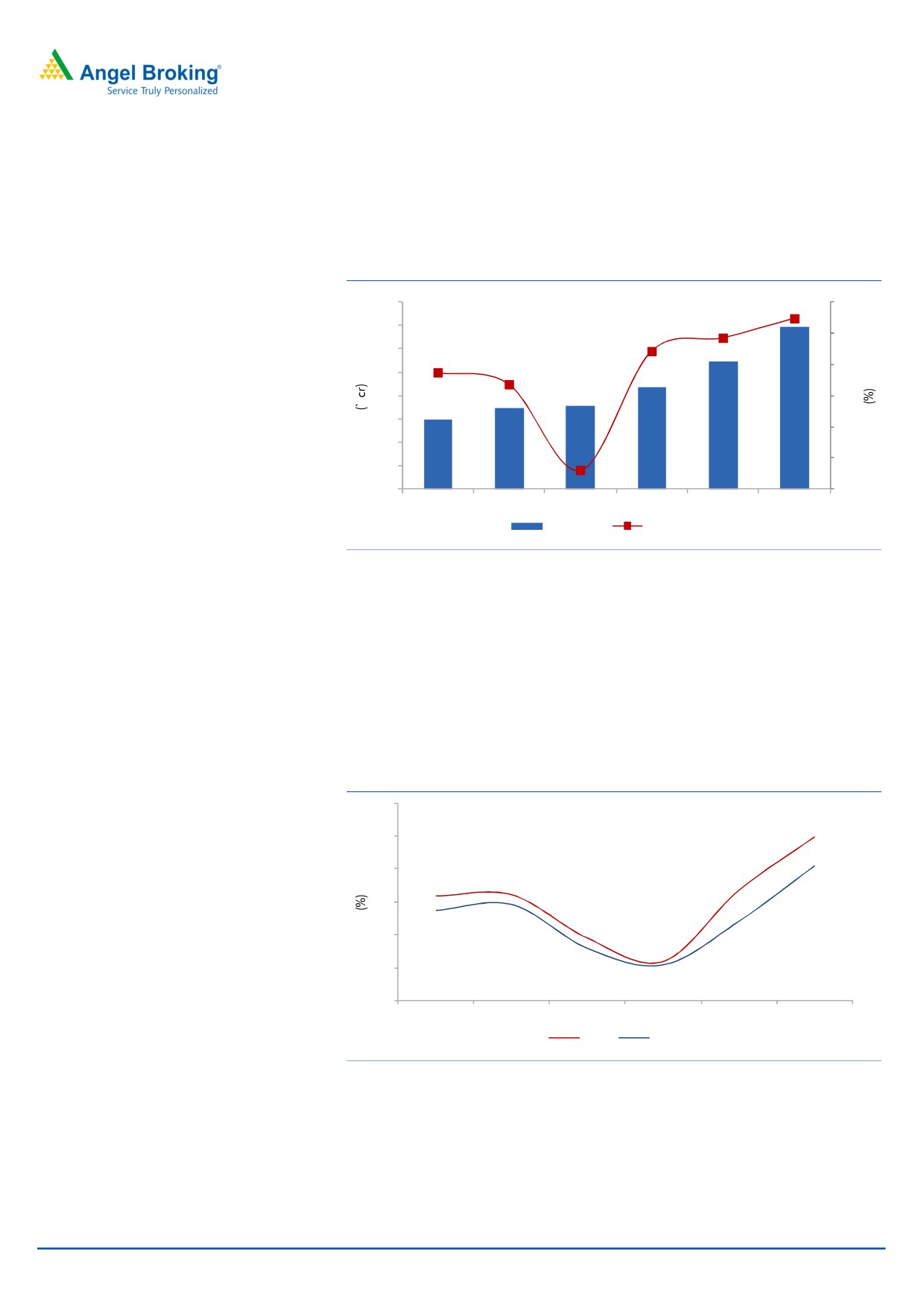

Company to report healthy consolidated growth

We expect ~25% CAGR in consolidated

We expect the company to post ~25% CAGR in net profit over FY2014-17E,

Net Profit over FY2014-17E

mainly led by strong revenue growth and improvement in margin.

Exhibit 18: Projected Net Profit growth trend

160

27.4

30

24.3

140

22.1

25

120

18.7

16.8

20

100

80

15

60

10

40

3.0

5

20

0

0

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

Net Profit

yoy growth (%)

Source: Company, Angel Research

Return ratios expected to bounce back

We expect the company to report improvement in its ROE and ROCE on the back

of healthy profitability with strong sales, healthy operating margin due to better

revenue segment mix, and higher utilization. In our view, the company is likely to

report a ROE of 14.6% to 17.1%and ROCE of 14.9% to 18.0% between FY2014 to

FY2017.

Exhibit 19: Improving ROE & ROCE

19

18

17

16

15

14

13

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

ROE

ROCE

Source: Company, Angel Research

February 21, 2015

12

Transport Corporation of India | Initiating Coverage

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Total operating income

2,132

2,228

2,468

2,830

3,350

% chg

9.0

4.5

10.8

14.6

18.4

Total Expenditure

1,957

2,058

2,271

2,581

3,049

Personnel Expenses

112

117

133

156

188

Others Expenses

1,845

1,941

2,137

2,425

2,861

EBITDA

175

170

198

249

302

% chg

10.6

(2.7)

16.3

25.9

21.1

(% of Net Sales)

8.2

7.6

8.0

8.8

9.0

Depreciation & Amortisation

46

47

54

63

73

EBIT

128

123

144

186

228

% chg

10.3

(4.0)

17.1

28.7

23.0

(% of Net Sales)

6.0

5.5

5.8

6.6

6.8

Interest & other Charges

34

31

33

36

38

Other Income

6

7

10

6

8

(% of PBT)

6.3

7.2

8.2

3.7

3.8

Share in profit of Associates

-

-

-

-

-

Recurring PBT

101

99

122

155

198

% chg

18.1

(1.8)

22.6

27.8

27.4

Prior Period & Extra. Exp./(Inc.)

-

-

-

-

-

PBT (reported)

101

99

122

155

198

Tax

32

27

34

47

59

(% of PBT)

31.2

27.7

28.0

30.0

30.0

PAT (reported)

70

72

88

109

139

Add: Share of earnings of asso.

-

-

-

-

-

Less: Minority interest (MI)

0

0

0

0

0

PAT after MI (reported)

70

72

87

109

138

ADJ. PAT

70

72

87

109

138

% chg

16.8

3.0

22.1

24.3

27.4

(% of Net Sales)

3.3

3.2

3.5

3.8

4.1

Basic EPS (`)

9.2

9.5

11.6

14.4

18.3

Fully Diluted EPS (`)

9.2

9.5

11.6

14.4

18.3

% chg

16.8

3.0

22.1

24.3

27.4

February 21, 2015

13

Transport Corporation of India | Initiating Coverage

Consolidated Balance sheet

Y/E March (` cr)

FY2013

FY2014

FY2015E FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

15

15

15

15

15

Reserves& Surplus

422

476

606

691

796

Shareholders Funds

437

491

621

706

811

Minority Interest

1

3

3

3

3

Total Loans

354

336

395

430

460

Deferred Tax Liability

32

33

33

33

33

Total Liabilities

824

863

1,052

1,172

1,307

APPLICATION OF FUNDS

Gross Block

652

693

823

973

1,123

Less: Acc. Depreciation

234

262

315

378

451

Net Block

418

432

508

595

672

Capital Work-in-Progress

5

18

18

18

18

Investments

8

8

8

8

8

Current Assets

534

543

677

731

828

Inventories

2

2

2

2

2

Sundry Debtors

395

380

419

481

569

Cash

46

43

120

85

53

Loans & Advances

67

65

74

91

114

Other Assets

24

53

62

74

90

Current liabilities

141

138

159

181

218

Net Current Assets

393

405

518

551

609

Mis. Exp. not written off

-

-

-

-

-

Total Assets

824

863

1,052

1,172

1,307

February 21, 2015

14

Transport Corporation of India | Initiating Coverage

Consolidated Cash flow

Y/E March (` cr)

FY2013

FY2014

FY2015E FY2016E FY2017E

Profit before tax

101

99

122

155

198

Depreciation

46

47

54

63

73

Change in Working Capital

(46)

15

(35)

(69)

(91)

Interest / Dividend (Net)

29

25

33

36

38

Direct taxes paid

(26)

(28)

(34)

(47)

(59)

Others

0

0

0

0

0

Cash Flow from Operations

104

158

138

140

159

(Inc.)/ Dec. in Fixed Assets

(55)

(98)

(130)

(150)

(150)

(Inc.)/ Dec. in Investments

(6)

-

-

-

-

Cash Flow from Investing

(61)

(98)

(130)

(150)

(150)

Issue of Equity

1

1

60

0

0

Inc./(Dec.) in loans

13

(19)

60

35

30

Dividend Paid (Incl. Tax)

(8)

(12)

(17)

(24)

(33)

Interest / Dividend (Net)

(35)

(33)

(33)

(36)

(38)

Cash Flow from Financing

(28)

(63)

69

(25)

(41)

Inc./(Dec.) in Cash

15

(3)

78

(35)

(32)

Opening Cash balances

31

46

43

120

85

Closing Cash balances

46

43

120

85

53

February 21, 2015

15

Transport Corporation of India | Initiating Coverage

Key Ratios

Y/E March

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

27.2

26.4

21.6

17.4

13.7

P/CEPS

16.3

15.9

13.4

11.0

8.9

P/BV

4.3

3.9

3.0

2.7

2.3

Dividend yield (%)

0.6

0.7

0.9

1.3

1.8

EV/Sales

1.0

1.0

0.9

0.8

0.7

EV/EBITDA

12.5

12.8

10.9

8.9

7.6

EV / Total Assets

2.3

2.2

1.8

1.6

1.5

Per Share Data (`)

EPS (Basic)

9.2

9.5

11.6

14.4

18.3

EPS (fully diluted)

9.2

9.5

11.6

14.4

18.3

Cash EPS

15.3

15.7

18.7

22.7

28.0

DPS

1.5

1.8

2.3

3.2

4.4

Book Value

57.8

64.9

82.1

93.3

107.2

Returns (%)

ROCE

16.2

14.9

14.2

16.4

18.0

Angel ROIC (Pre-tax)

17.4

15.9

16.3

17.8

18.9

ROE

15.9

14.6

14.1

15.4

17.1

Turnover ratios (x)

Asset Turnover (Gross Block)

5.1

5.2

4.9

4.8

5.0

Inventory / Sales (days)

0

0

0

0

0

Receivables (days)

68

62

62

62

62

Payables (days)

15

13

13

12

12

WC cycle (days)

53

50

49

50

50

Solvency ratios (x)

Net debt to equity

0.7

0.6

0.4

0.5

0.5

Net debt to EBITDA

1.7

1.7

1.3

1.5

1.4

Interest Coverage (EBIT / Int.)

3.8

4.0

4.4

4.8

5.7

February 21, 2015

16

Transport Corporation of India | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Transport Corporation of India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

February 21, 2015

17

Transport Corporation of India | Initiating Coverage

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research (Banking)

Amarjeet Maurya

Analyst (FMCG, Media, Mid-Cap)

Bharat Gianani

Analyst (Automobile, Auto Ancillary)

Rahul Dholam

Analyst (Metal, Oil & Gas)

Santosh Yellapu

Analyst (Infrastructure)

Shrenik Gujrathi

Analyst (Cap Goods, Cement)

Umesh Matkar

Analyst (Banking)

Twinkle Gosar

Analyst (Mid-Cap)

Neha Sinha

Economist

Tejas Vahalia

Research Editor

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Sneha Seth

Associate (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Assistant Manager

Production Team:

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

February 21, 2015

18